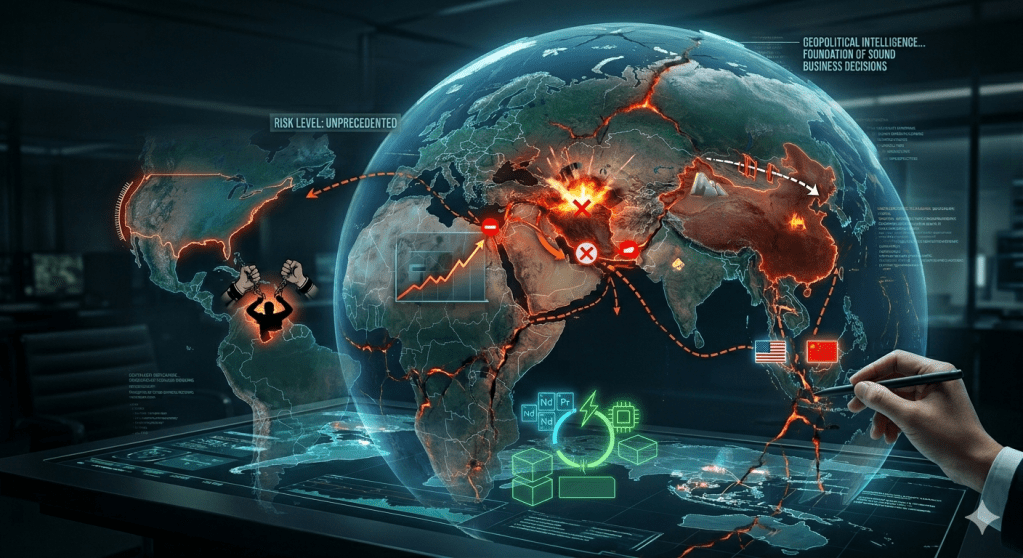

Q1 2026 did not ease in gently. The first three months of the year delivered a sequence of shocks that would have been considered unthinkable in any previous year, but increasingly looks like the new normal.

On 3 January, US forces arrested Venezuelan President Nicolás Maduro following airstrikes on military sites in Caracas, upending the politics of the Western Hemisphere overnight and putting the world’s largest proven oil reserves into play. Then, on 28 February, the US and Israel launched coordinated strikes on Iran, killing Supreme Leader Ali Khamenei and triggering an oil price shock that sent Brent crude surging past $120 per barrel. The Strait of Hormuz, the corridor through which roughly a fifth of the world’s oil and LNG flows, was effectively closed, sending global markets into further disarray.

The energy price shock was immediate. The downstream effects on manufacturing, agriculture, logistics, and AI infrastructure are far reaching and still unfolding.

Meanwhile, the trade environment in Asia remained anything but stable. The Trump administration’s tariff regime, a blanket 10% global levy compounded by accelerating Section 301 investigations, continued to squeeze Southeast Asian exporters. Countries that had moved swiftly to sign bilateral agreements with Washington found their advantages eroding much faster than anticipated. For the region’s major economies, the old export-led growth model that has served the region well in the past is now under heavy pressure.

The planned Trump-Xi summit from 31 March to 2 April, a potential reset in the world’s most consequential bilateral relationship, was officially postponed to May, with Trump citing the Iran conflict as the reason. The delay, rather than cancellation, suggests neither side wants to abandon diplomacy entirely. But the relationship is increasingly subject to external shocks that neither Washington nor Beijing can fully control.

On the technology front, the contest for control over the energy, critical minerals, and chips that power artificial intelligence – what we termed the “21st century resources war” – accelerated sharply in Q1. In February, Washington convened 54 nations at its inaugural Critical Minerals Ministerial, launching Project Vault, a $12 billion strategic stockpile, and announcing FORGE, a new global partnership designed to set price floors and create a preferential trading zone for critical minerals, explicitly to counter China’s dominance over mining and processing.

China, for its part, has not been shy about using its leverage from controlling roughly 70% of global rare earth mining sources and 90% of processing capacity. And thus, the rare earth export controls imposed by Beijing in April 2025 remained in place. For Southeast Asian governments caught between both powers, the pressure to align is mounting – Malaysia and Thailand both signed critical minerals MOUs with Washington, drawing immediate scrutiny at home and counter-pressure from Beijing.

These complex geopolitical dynamics are unlikely to ease up anytime soon. Instead they are growing increasingly unpredictable and harder to navigate. Q1 of 2026 has illustrated why geopolitical intelligence is not a luxury – it is the foundation of sound business decisions.

If your company or organisation has exposure in Asia, talk to us and we’ll find out how we can help you navigate these turbulent times.

Leave a comment